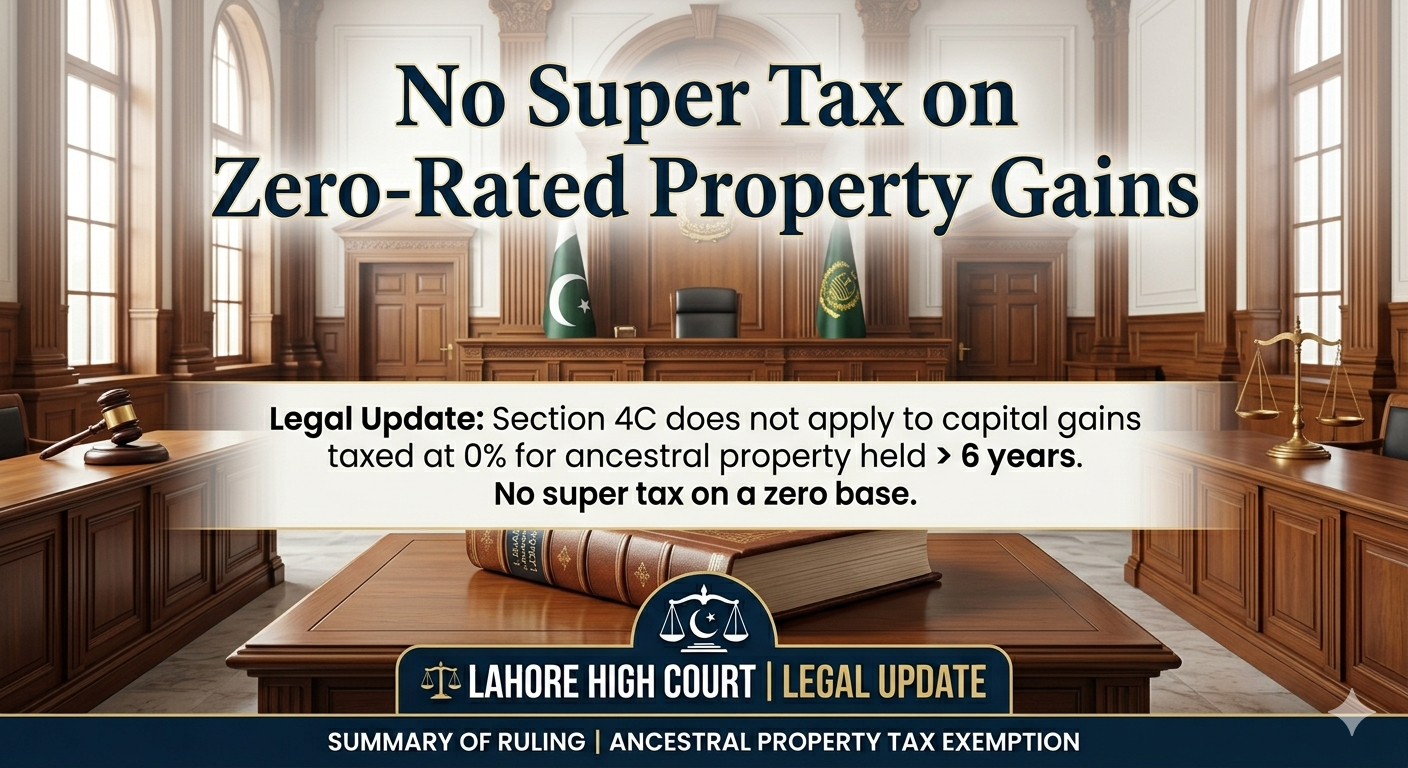

Super Tax Pakistan, Section 4C exemption, Capital Gains tax 0%, Lahore High Court judgment, ancestral property tax, Section 37(1A) Description: The Lahore High Court rules that Super Tax cannot be applied to capital gains from ancestral property held over six years, as a 0% tax rate leaves no base for supplementary levies.

Read More

A recent Lahore Appellate Tribunal ruling clarifies that businesses can use current year losses to lower their Super Tax under Section 4C. This decision prevents tax officials from taxing gross profits while ignoring real operational losses, ensuring a fairer calculation of total taxable income.

Read More

The SECP has issued a final warning for companies to disclose their ultimate beneficial owners by April 30. Using Form-19, businesses must identify who truly controls their operations to avoid heavy fines. This initiative is part of a broader push to increase corporate transparency and fight financial crime in Pakistan.

Read More

A recent Appellate Tribunal Inland Revenue (ATIR) ruling clarifies that tax authorities cannot directly demand Super Tax under Section 4C if a tax return is already deemed assessed . Instead, they must follow the formal amendment process under Section 122, or the orders will be considered legally void . S

Read More

Understand the Federal Board of Revenue's (FBR) STGO 01 of 2026. This guide details the shift toward using multiple licensed integrators and the strict 72-hour window for editing electronic sales tax invoices, providing vital compliance insights for Pakistani businesses and tax practitioners.

Read More

While the Partnership Act, 1932 allows partners to mutually agree on salaries, the Income Tax Ordinance, 2001 imposes strict prohibitions. Understanding Section 21(j) is vital for business owners and tax practitioners to avoid unexpected tax liabilities when compensating members of an Association of Persons (AOP).

Read More

Many taxpayers fear the FBR will tax profits from selling personal vehicles. However, a landmark ruling in ITA No. 31/IB/2026 confirms that under Section 37(5) of the Income Tax Ordinance, 2001, personal movable property is exempt from capital gains tax, and the authorities cannot use residual clauses to bypass this exclusion.

Read More

Discover how builders and developers under the Section 7F special tax regime can resolve liquidity issues. This guide explains the process of obtaining a Section 159 exemption certificate to prevent the collection of Section 236C advance tax on property sales.

Read More

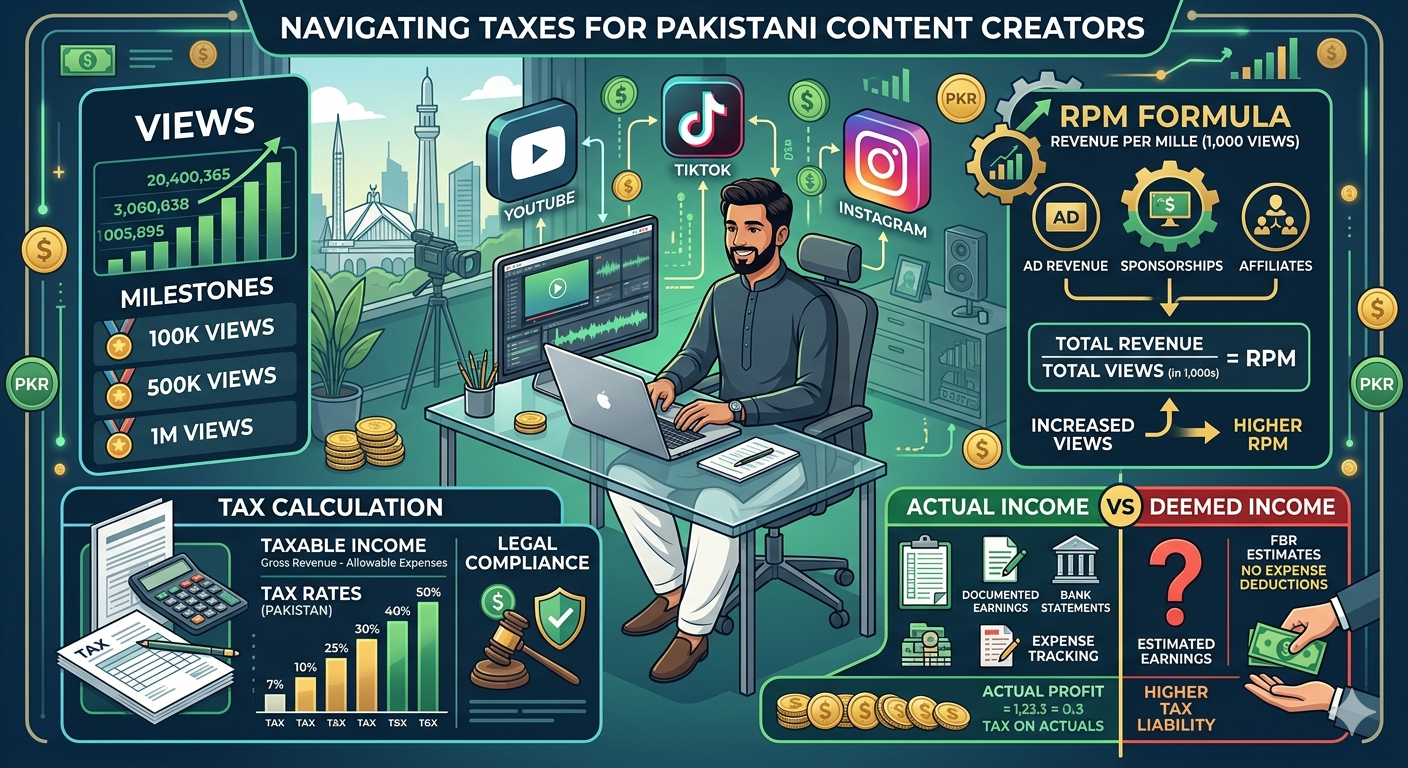

A practical guide explaining Pakistan’s new taxation rules for social media income under the Income Tax Ordinance, 2001. Covers legal provisions, computation method, comparison with existing law, and critical analysis of the FBR’s presumptive approach for content creators.

Read More

Learn how salaried employees in Pakistan can use the IT-3 Form to claim tax credits on mobile bills, vehicle tax, and more to increase monthly take-home pay.

Read More

Can partners take salary from an AOP in Pakistan? Learn the legal position under the Partnership Act, 1932 and its tax treatment under the Income Tax Ordinance, 2001.

Read More

The launch of PRA IRIS was intended to herald a new era in sales tax filing for taxpayers in Punjab. However, the initial experience has highlighted several areas where the portal falls short of expectations. By addressing these issues promptly, the Punjab Revenue Authority can deliver on its promise of providing a streamlined and user-friendly tax filing experience. Until then, it remains to be seen whether PRA IRIS will live up to its name as "A NEW EXPERIENCE" or simply be seen as more of the same.

Read More

Copyright @ Taxationist. Designed By TechWare House