A practical guide explaining Pakistan’s new taxation rules for social media income under the Income Tax Ordinance, 2001. Covers legal provisions, computation method, comparison with existing law, and critical analysis of the FBR’s presumptive approach for content creators.

With the rapid growth of digital content creation, Pakistan’s tax regime is now attempting to formally capture income generated through platforms like YouTube, TikTok, and Instagram. The recent draft rules introduce a formula-based taxation model, raising a fundamental question: can estimated income replace actual earnings in a dynamic digital economy?

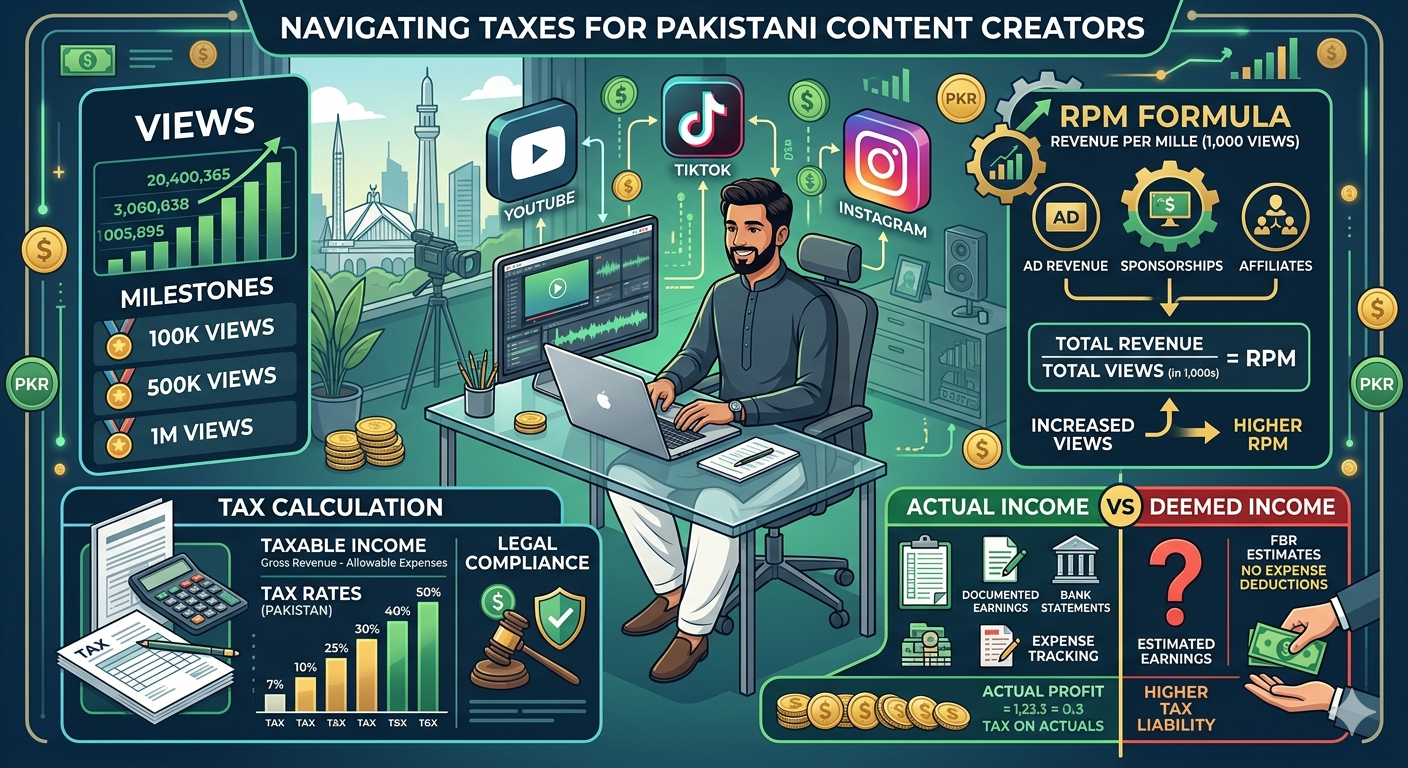

The proposed regime is introduced under Section 99C read with Section 237 of the Income Tax Ordinance, 2001, allowing the Federal Board of Revenue (FBR) to prescribe special procedures for certain classes of income. The mechanism also interacts with Section 147 (advance tax) and overlaps with Section 154A, which already governs withholding on digital payments.

The rules introduce a minimum income formula based on RPM (Revenue per Mille), capping expenses at 30% and taxing the higher of actual or deemed income.

The initiative reflects a positive step toward documentation of the digital economy. It may help broaden the tax base, capture undocumented income streams, and create a standardized compliance framework for content creators who previously operated outside formal taxation.

However, the model suffers from structural flaws. It assumes a fixed RPM across all creators, ignoring variations in audience geography, niche, and monetization models. This contradicts the principle of taxation on real income. The 30% expense cap is arbitrary and may lead to taxation of gross receipts rather than net profit.

Moreover, duplication with Section 154A raises concerns of double taxation, while empowering the Commissioner to “rectify” returns based on estimates challenges due process and legal boundaries.

Creators should maintain detailed records of actual income, audience analytics, and expenses to defend their position against deemed assessments. While the rules aim at compliance, their practical implementation may lead to disputes unless refined. A balanced approach focusing on actual receipts and platform-level reporting would be more aligned with global practices.

Copyright @ Taxationist. Designed By TechWare House