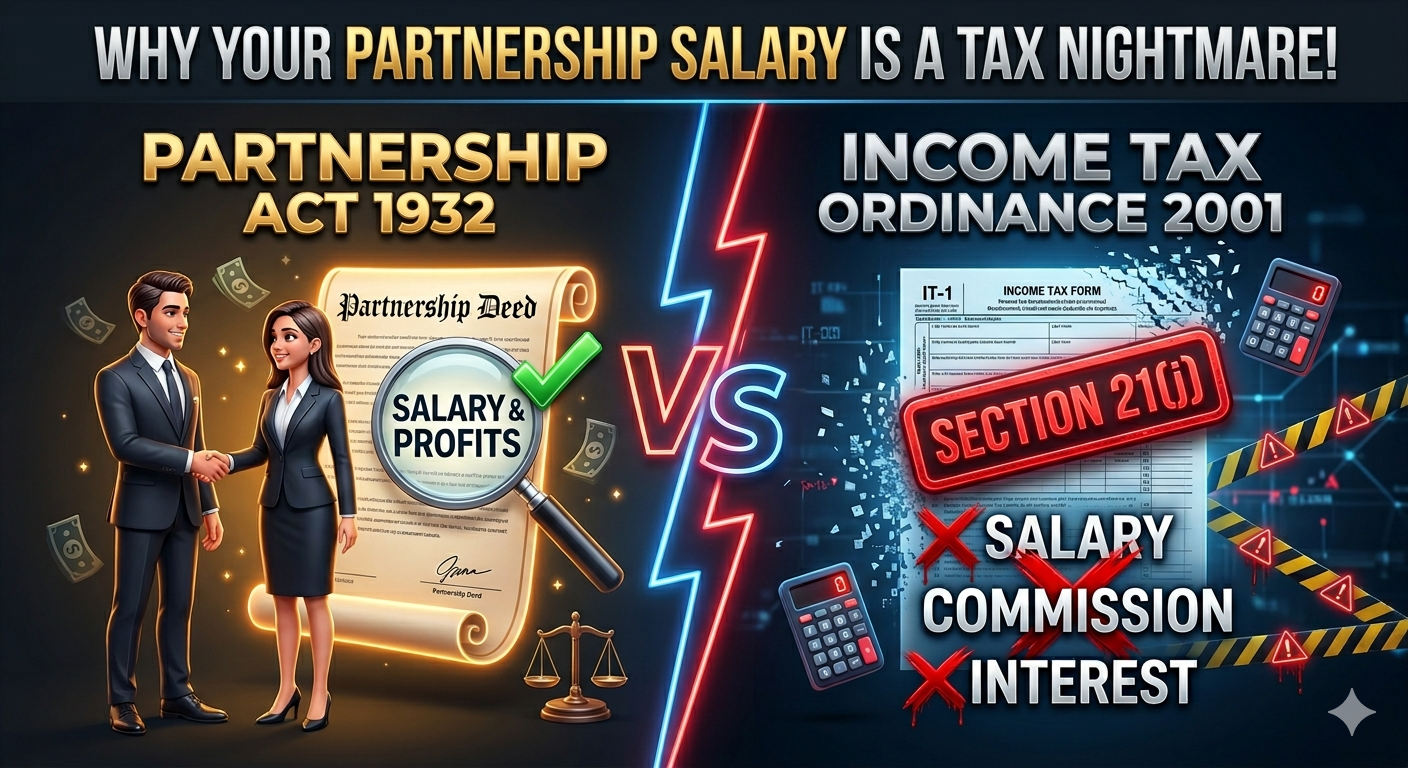

In Pakistan’s SME landscape, the

Association of Persons (AOP) remains a widely adopted business structure. A

recurring issue arises where active partners, who manage day-to-day operations,

expect compensation in the form of a salary. While this appears commercially

justified, it creates a legal and tax conflict: what is contractually valid

under partnership law is not necessarily recognized as a deductible expense

under tax law.

Legal

Position under the Partnership Act, 1932

The Partnership Act, 1932 provides

flexibility to partners in structuring their internal arrangements. Under

Section 11, partners may determine their rights and obligations through mutual

agreement. Further, Section 13(a) clarifies that although a partner is not

automatically entitled to remuneration, such entitlement can arise through a

contract to the contrary, typically documented in the partnership deed.

Accordingly, a partner may legally

receive salary if explicitly agreed upon by all partners.

Tax

Treatment under the Income Tax Ordinance, 2001

The position shifts significantly

under tax law. Section 21(j) of the Income Tax Ordinance, 2001 expressly

disallows any deduction for salary, commission, brokerage, or other

remuneration paid by an AOP to its members when computing taxable business

income.

From a tax perspective, these

payments are treated not as business expenses but as appropriation of profit.

Consequently, even if such payments are contractually valid and actually

disbursed, they must be added back to the AOP’s taxable income.

Wider

Compliance Considerations

While income tax law governs

deductibility, practitioners should also consider the Sales Tax Act, 1990 and

relevant provincial service tax laws. Generally, a partner’s services to the

AOP are regarded as internal management functions rather than taxable supplies.

However, registration and compliance obligations should still be evaluated

based on the nature of business activities.

Critical

Analysis

Advantages:

- Ensures fair compensation for working partners

- Provides flexibility in structuring profit-sharing

arrangements

Disadvantages:

- Increases taxable income due to the disallowance of

partner remuneration

- Creates a mismatch between accounting profit and

taxable income

Policy Perspective:

While the law may appear rigid, it aims to prevent tax avoidance through

artificial reduction of profits by allocating excessive remuneration to

partners.

Conclusion:

Practical Takeaway

The legal position is unequivocal:

contractual entitlement does not determine tax deductibility. Partners may

agree on salaries under the Partnership Act, 1932; however, under the Income

Tax Ordinance, 2001, such payments are not allowable deductions and are treated

as part of the AOP’s taxable profit.

For practitioners and business

owners, this requires careful tax planning, recognizing that partner salary is

effectively a distribution of profit in the eyes of tax authorities, not a

deductible business expense.